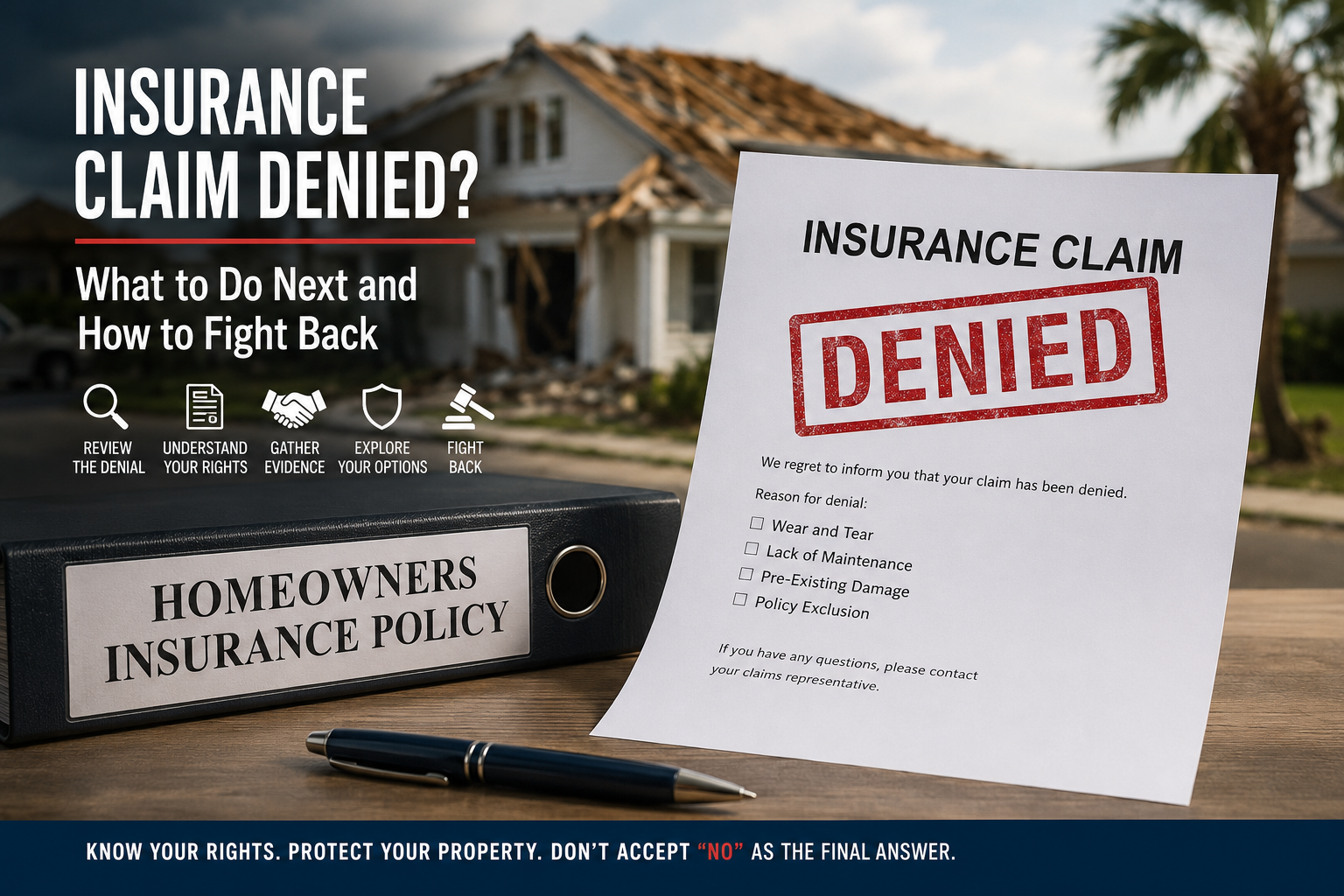

Insurance Claim Denied? What to Do Next and How to Fight Back Against an Unfair Denial

Receiving a denial letter from your insurance company can feel overwhelming, but a denial doesn't always mean your claim is over. Learn the most common reasons claims are denied, what your options are, and how homeowners can challenge unfair decisions through additional evidence, supplements, appraisal, and professional representation.

From Stove Fire to Full Property Claim: Understanding the True Cost of Smoke and Soot Damage

A kitchen fire might seem like a small incident—but the smoke, soot, and chemical damage can affect every room in your home. Learn why fire marshal reports, hygienist testing, and public adjusters are essential after even the smallest blaze.

8 Things to Look For in Your Homeowners Insurance Policy

Most homeowners only learn what their insurance doesn't cover after it's too late. Don’t wait for a denied claim to discover your policy’s weak spots. This guide explains 8 critical policy elements every Florida homeowner should review before disaster strikes—from appraisal clauses to roof replacement cost coverage.

What to Do If Your Condo Association’s Insurance Isn’t Covering Your Unit’s Damage

If your condo suffers damage and the HOA’s insurance won’t pay, you may be left in limbo. This blog explains what’s covered under the master policy vs. your personal policy, and how to recover losses with help from a public adjuster.