The first 24 hours after a house fire are some of the most important for both your family's safety and your insurance claim. Learn the essential steps homeowners should take to protect their property, preserve evidence, document damage, and begin the recovery process.

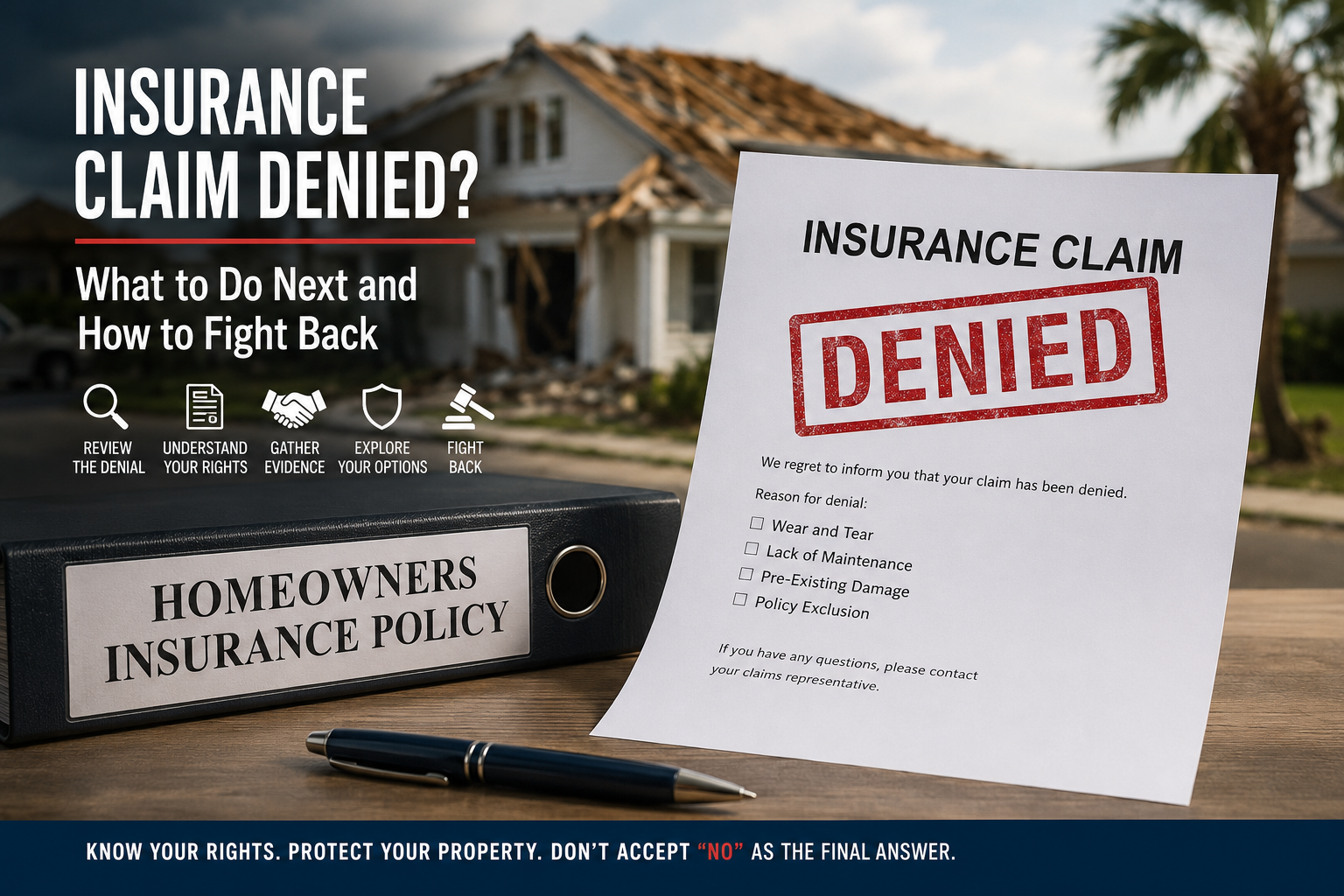

Receiving a denial letter from your insurance company can feel overwhelming, but a denial doesn't always mean your claim is over. Learn the most common reasons claims are denied, what your options are, and how homeowners can challenge unfair decisions through additional evidence, supplements, appraisal, and professional representation.

June 1 is the official start of hurricane season. Beyond food, water, and safety planning, homeowners and business owners should prepare from an insurance claim perspective. Learn how to document your property, review your policy, understand deductibles, avoid bad coverage, and protect your claim before the next storm.

How long an insurance claim takes depends on the type of loss, the insurance company, the policy, the documentation needed, and whether the claim is accepted, underpaid, partially denied, or denied in full. Here’s what property owners should understand about insurance claim timelines, supplements, disputes, and why patience is often required.

VIP Adjusting is proud to congratulate Cristian Bragano, our Director of Claims and Licensed Public Adjuster, on earning his Florida Certified Building Contractor’s license. This achievement reflects Cristian’s continued professional growth and further strengthens the depth of expertise we bring to the policyholders we represent.

VIP Adjusting is now providing Public Adjuster services in Dallas, Fort Worth, and the greater DFW area, helping property owners handle insurance claims involving storm damage, water damage, fire losses, and other property-related issues. If you are searching for a Dallas Public Adjuster or Fort Worth Public Adjuster, our team is available to assist with inspections, estimates, and claim representation.

Learn what a supplemental insurance claim is, why claims are often underpaid, and how additional funds may still be available after your initial settlement.

Homeowners affected by Hurricane Milton in Florida have until April 9, 2026 to file a supplemental claim. Find out if your insurance claim was underpaid and what steps to take before the deadline.

When riots or civil unrest lead to property damage, most homeowners and business owners are unsure if their insurance will pay. This blog breaks down how insurance companies classify riot-related events, when damage may be covered, and how to protect your rights in the event of widespread chaos. Read before the next unexpected event strikes.

The first 24 hours after a house fire are some of the most important for both your family's safety and your insurance claim. Learn the essential steps homeowners should take to protect their property, preserve evidence, document damage, and begin the recovery process.