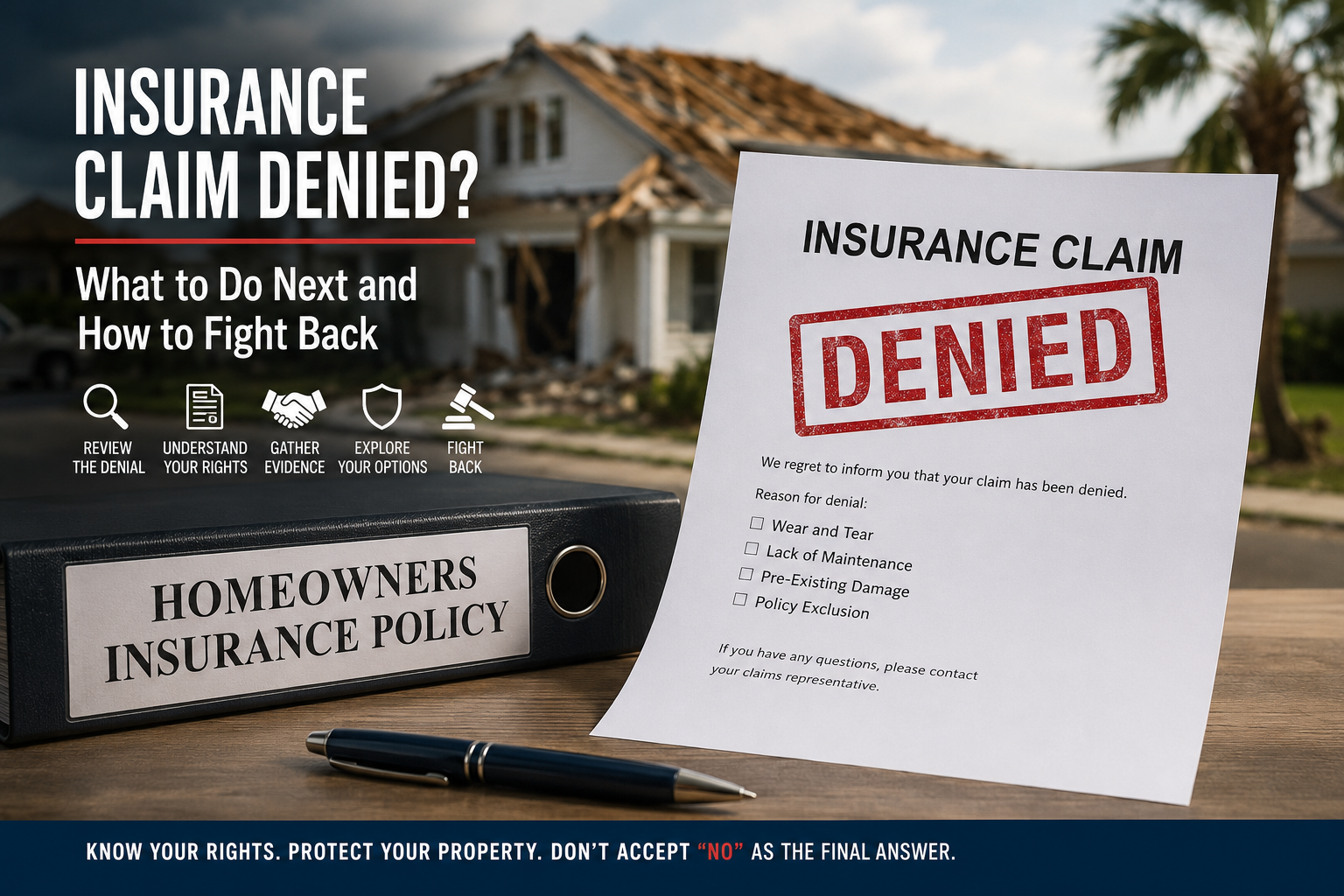

Insurance Claim Denied? What to Do Next and How to Fight Back Against an Unfair Denial

Receiving a denial letter from your insurance company can feel overwhelming, but a denial doesn't always mean your claim is over. Learn the most common reasons claims are denied, what your options are, and how homeowners can challenge unfair decisions through additional evidence, supplements, appraisal, and professional representation.