House Fire Insurance Claim: What to Do in the First 24 Hours

The first 24 hours after a house fire are some of the most important for both your family's safety and your insurance claim. Learn the essential steps homeowners should take to protect their property, preserve evidence, document damage, and begin the recovery process.

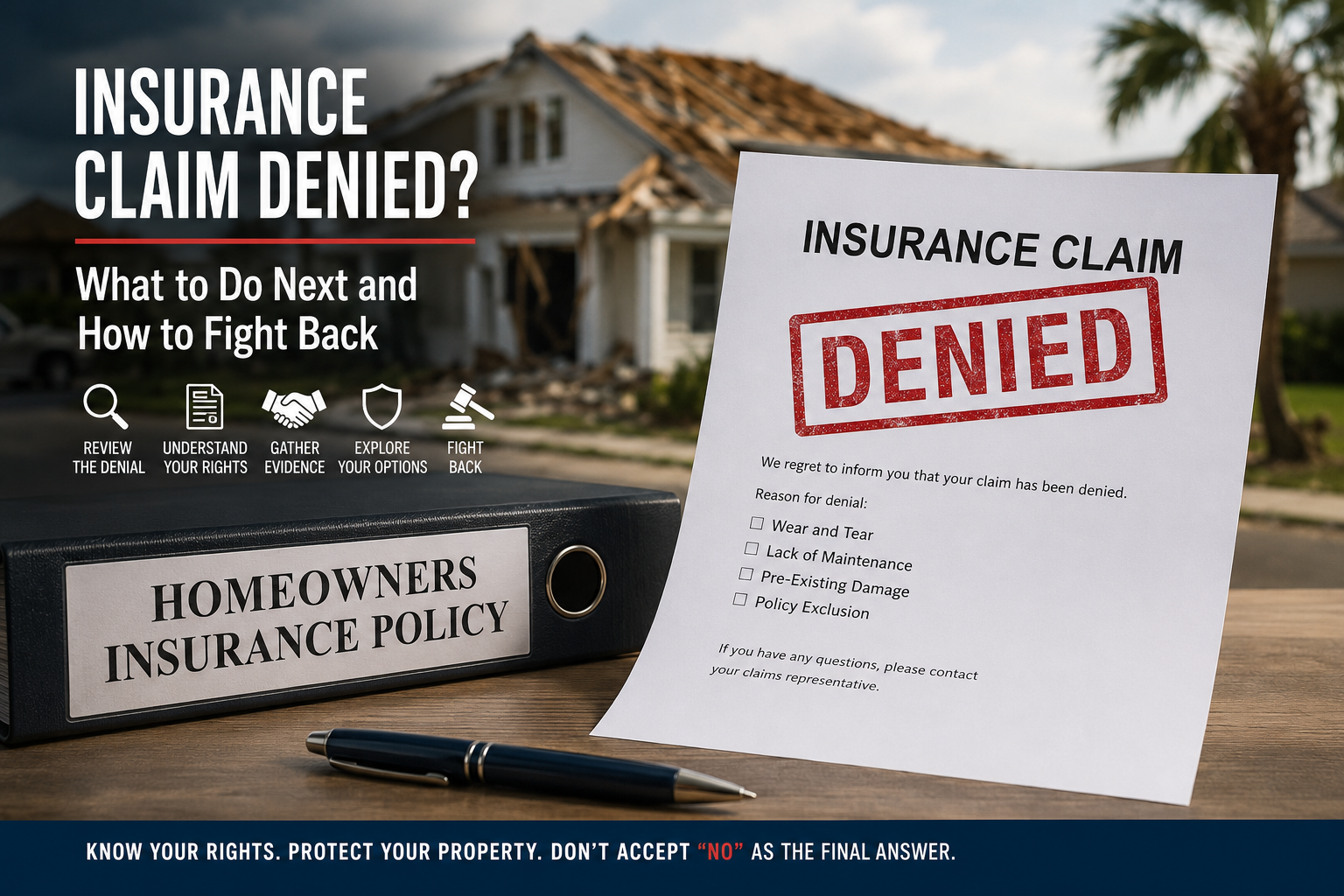

Insurance Claim Denied? What to Do Next and How to Fight Back Against an Unfair Denial

Receiving a denial letter from your insurance company can feel overwhelming, but a denial doesn't always mean your claim is over. Learn the most common reasons claims are denied, what your options are, and how homeowners can challenge unfair decisions through additional evidence, supplements, appraisal, and professional representation.

Hurricane Season Starts Today: Be Prepared Before the Storm

June 1 is the official start of hurricane season. Beyond food, water, and safety planning, homeowners and business owners should prepare from an insurance claim perspective. Learn how to document your property, review your policy, understand deductibles, avoid bad coverage, and protect your claim before the next storm.

Congratulations to Cristian Bragano on Becoming a Licensed Florida Contractor

VIP Adjusting is proud to congratulate Cristian Bragano, our Director of Claims and Licensed Public Adjuster, on earning his Florida Certified Building Contractor’s license. This achievement reflects Cristian’s continued professional growth and further strengthens the depth of expertise we bring to the policyholders we represent.

Dallas Public Adjuster Services | VIP Adjusting Now Serving DFW

VIP Adjusting is now providing Public Adjuster services in Dallas, Fort Worth, and the greater DFW area, helping property owners handle insurance claims involving storm damage, water damage, fire losses, and other property-related issues. If you are searching for a Dallas Public Adjuster or Fort Worth Public Adjuster, our team is available to assist with inspections, estimates, and claim representation.

From Stove Fire to Full Property Claim: Understanding the True Cost of Smoke and Soot Damage

A kitchen fire might seem like a small incident—but the smoke, soot, and chemical damage can affect every room in your home. Learn why fire marshal reports, hygienist testing, and public adjusters are essential after even the smallest blaze.

8 Things to Look For in Your Homeowners Insurance Policy

Most homeowners only learn what their insurance doesn't cover after it's too late. Don’t wait for a denied claim to discover your policy’s weak spots. This guide explains 8 critical policy elements every Florida homeowner should review before disaster strikes—from appraisal clauses to roof replacement cost coverage.

10 “Did You Know?” Facts About Property Insurance Claims That Could Save You Thousands

Don’t let insurance policy fine print cost you thousands. Discover 10 surprising facts that can impact your claim—and how VIP Adjusting can help you recover what you’re truly owed.

How Insurance Companies Delay or Deny Legitimate Claims - What You Can Do About It

Florida law now requires insurance companies to respond to your property damage claim within 60 days—not 90. If your claim is sitting in limbo, you may have legal leverage. Learn what the statute says and how VIP Adjusting can help protect your rights.

What to Consider When Buying a Property with an Open Insurance Claim

When buying a property with an ongoing insurance claim, understanding the claim’s impact is crucial. From Assignment of Benefits (AOB) transfers to securing new insurance, VIP Adjusting helps you navigate the complexities, ensuring the claim is fairly adjusted and your investment is fully protected. Let us guide you through the process and maximize your claim settlement.