What is a Supplemental Insurance Claim?

After an insurance company makes their initial determination on a claim, many homeowners assume the process is complete. In reality, there are many situations where additional funds may still be owed.

This is where a supplemental claim comes into play.

What Is a Supplemental Claim?

A supplemental claim is a request for additional payment on an existing insurance claim when the insurance company's determination does not fully cover the damage. It is not a new claim, but an extension of the original claim. This typically happens when additional damage becomes more apparent over time or when the cost of repairs exceeds the initial estimate.

Real Example: Initial Claim vs. Supplemental Outcome

Below is an example of a claim in Englewood, Florida following Hurricane Ian, where the initial insurance determination resulted in no payment, followed by a supplemental claim that significantly changed the outcome.

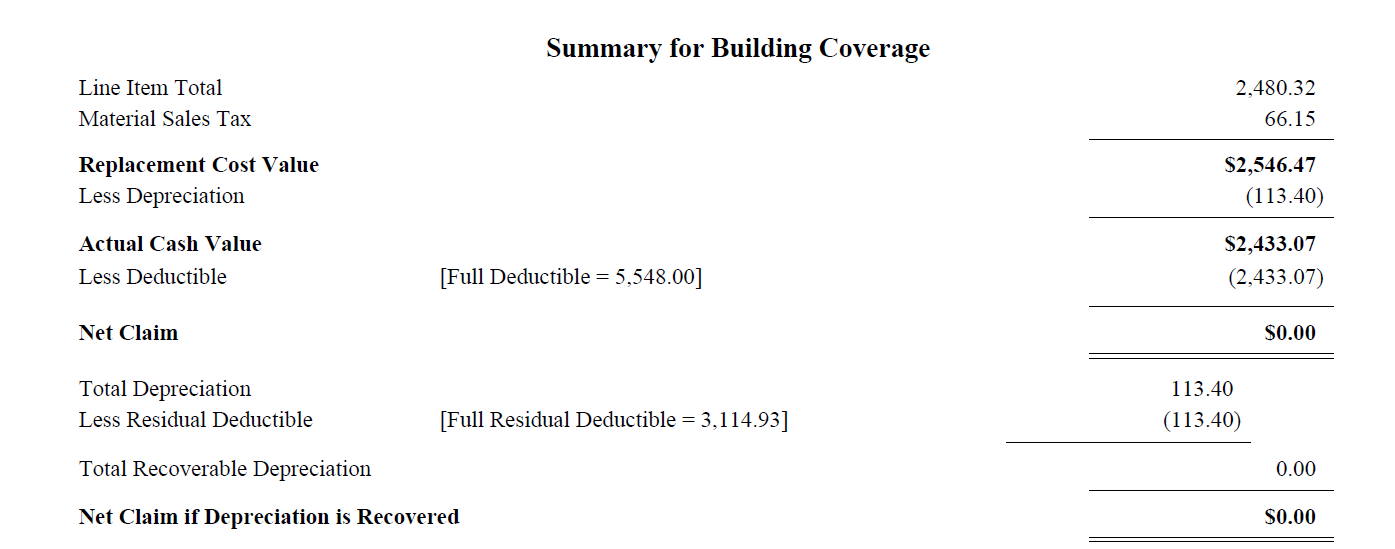

Initial Claim Determination

As shown in the carrier’s original estimate below, the insurance company valued the loss at approximately $2,433.07 actual cash value, which fell below the policy deductible of $5,548.00.

Because of this, the net claim payment was $0.00, and the claim was closed by the insurance company despite the presence of damage.

The insurance company’s initial determination on the claim which came in below the deductible, resulting in no payment being issued.

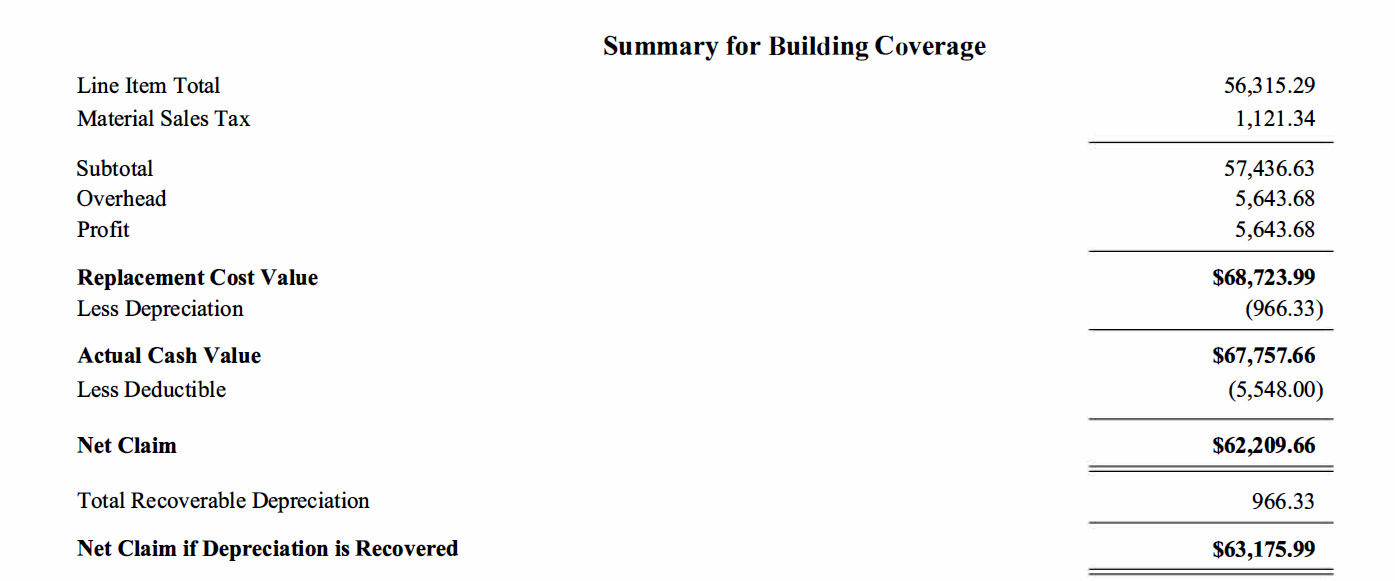

After Supplemental Claim Review

After being retained to review the claim, VIP Adjusting conducted a detailed evaluation of the original estimate, inspected the property for additional damage, and produced a comprehensive estimate reflecting the full scope of loss. A supplemental claim was then filed to address items that were missed or underpaid.

The revised estimate increased the replacement cost value to $68,723.99, resulting in a net claim payment of $62,209.66 after the deductible and recoverable depreciation were applied.

The supplemental estimate included payment for a full roof replacement, fencing, and multiple interior rooms throughout the home, none of which were included in the insurance company’s original determination.

This is a clear example of how a claim that initially resulted in no payment can change significantly when properly evaluated and documented.

The insurance company’s revised determination after VIP Adjusting assisted in pursuing a supplemental claim.

Why Supplemental Claims Are Common

When most homeowners receive their initial determination from their insurance company, many are left wondering whether that is all they are entitled to recover. Others may suspect the claim was underpaid but are unsure how to demonstrate that to the insurance company.

In many situations, the full extent of damage is not identified during the insurance company’s initial evaluation. What may appear to be a minor or repairable issue can require more extensive work once repairs begin or the property is reviewed in greater detail. In other cases, the damage may affect a continuous surface and require full replacement due to repairability limitations or matching requirements.

It is also common for portions of the damage to be missed entirely, especially during high-volume storm situations where insurance company inspections are completed quickly. Most insurance companies take the position that it is the policyholder’s responsibility to identify and point out the damage to their field adjuster. Most homeowners are unaware of this and rely on the insurance company’s field adjuster to fully investigate the loss. This can often lead to a substantial amount of damage being missed and not included in the initial determination.

In other cases, the issue is not missed damage, but an incomplete or underpriced estimate. Insurance companies rely on standardized pricing and limited initial information, which does not always reflect real-world contractor costs. As repair estimates and invoices come in, the gap between what was paid and what is actually required becomes clear.

This is where a supplemental insurance claim becomes necessary.

However, identifying what was missed and properly documenting it in a way the insurance company will accept is not always straightforward. Most homeowners are not familiar with the level of detail, formatting, and support required to reopen or supplement a claim.

That is where professional representation can make a meaningful difference.

How We Can Help

A Public Adjuster can review your claim to determine whether anything was missed or underpaid.

At VIP Adjusting, we analyze your policy, your original estimate, and any repair documentation to identify gaps between what was paid and what is actually required to complete the work properly. As part of that process, we conduct our own inspection and prepare a detailed estimate reflecting the full scope of damage.

One of the biggest issues we see is the disconnect between contractor estimates and insurance estimates. Contractors are focused on completing the job to the customer’s satisfaction, not writing estimates in insurance-approved formats or line-item structures. Their proposals may also include upgrades or items that are not covered under the policy.

On the other side, insurance companies evaluate estimates using specific pricing databases, scope requirements, and strict documentation standards based on what is covered under the policy. Because contractor estimates are not prepared with these standards in mind, they are often reduced, challenged, or rejected altogether.

We help bridge that gap.

If additional funds are owed, we prepare and submit the supplemental claim with proper documentation, insurance-compliant formatting, and a clearly defined scope of work. We also work directly with contractors, review invoices, and present the claim in a way the insurance company can properly evaluate.

Our role is to level the playing field and ensure your claim reflects the true cost of your loss.

Reopened Claim vs. Supplemental Claim

Some states, including Florida, make a distinction between a reopened claim and a supplemental claim.

A reopened claim typically involves requesting additional payment for damage that was already known and previously reported.

A supplemental claim involves additional or newly discovered damage related to the same loss.

While the terms are sometimes used interchangeably, the distinction can matter depending on the policy and state.

Do Supplemental Claims Have Deadlines?

Yes, and this is one of the most important factors.

Deadlines vary by state and policy, but they are always enforced.

For example, in Florida, recent changes have shortened the timeframe:

1 year to report an initial or reopened claim

18 months to file a supplemental claim

Other states may allow more time, but the key takeaway is the same: waiting too long can limit or eliminate your ability to recover additional funds.

When Should You File a Supplemental Insurance Claim?

Supplemental claims are typically filed when:

Additional damage is discovered, sometimes after repairs begin

The insurance company’s original estimate did not include the full scope of work

Repair costs come in higher than expected

For example, a roof may appear repairable during the initial inspection, but once work begins, it becomes clear that a full replacement is necessary. That difference can be submitted as a supplemental claim.

You should also consider filing a supplemental claim if your insurance payment does not reflect the true cost of repairs, or if the original estimate appears incomplete or underestimated.

Even if repairs have already been completed, a supplemental claim may still be possible depending on timing and documentation.

Final Thought

A supplemental insurance claim exists to ensure your settlement reflects the full extent of your loss, not just what was identified during the initial inspection.

If your insurance claim was underpaid, incomplete, or does not reflect the true cost of repairs, it may be worth having it reviewed before applicable deadlines pass.

Working with a Public Adjuster can help identify missed or underpaid damage, properly document the claim, and present a supplemental claim in a way the insurance company can fully evaluate.

If you have questions or would like a free review of your claim, feel free to contact our office.